What You Need to Know About RRIFs

What You Need to Know About RRIFs: Turning Your RRSP Into Retirement Income

As retirement approaches, many Canadians start wondering: what happens to all the savings they’ve been building in their RRSP? The good news is, your RRSP doesn’t just stop working for you when you turn 71. Instead, it can be converted into a Registered Retirement Income Fund (RRIF)—a flexible way to draw steady income while keeping your investments working.

What is an RRIF, and how is it different from an RRSP?

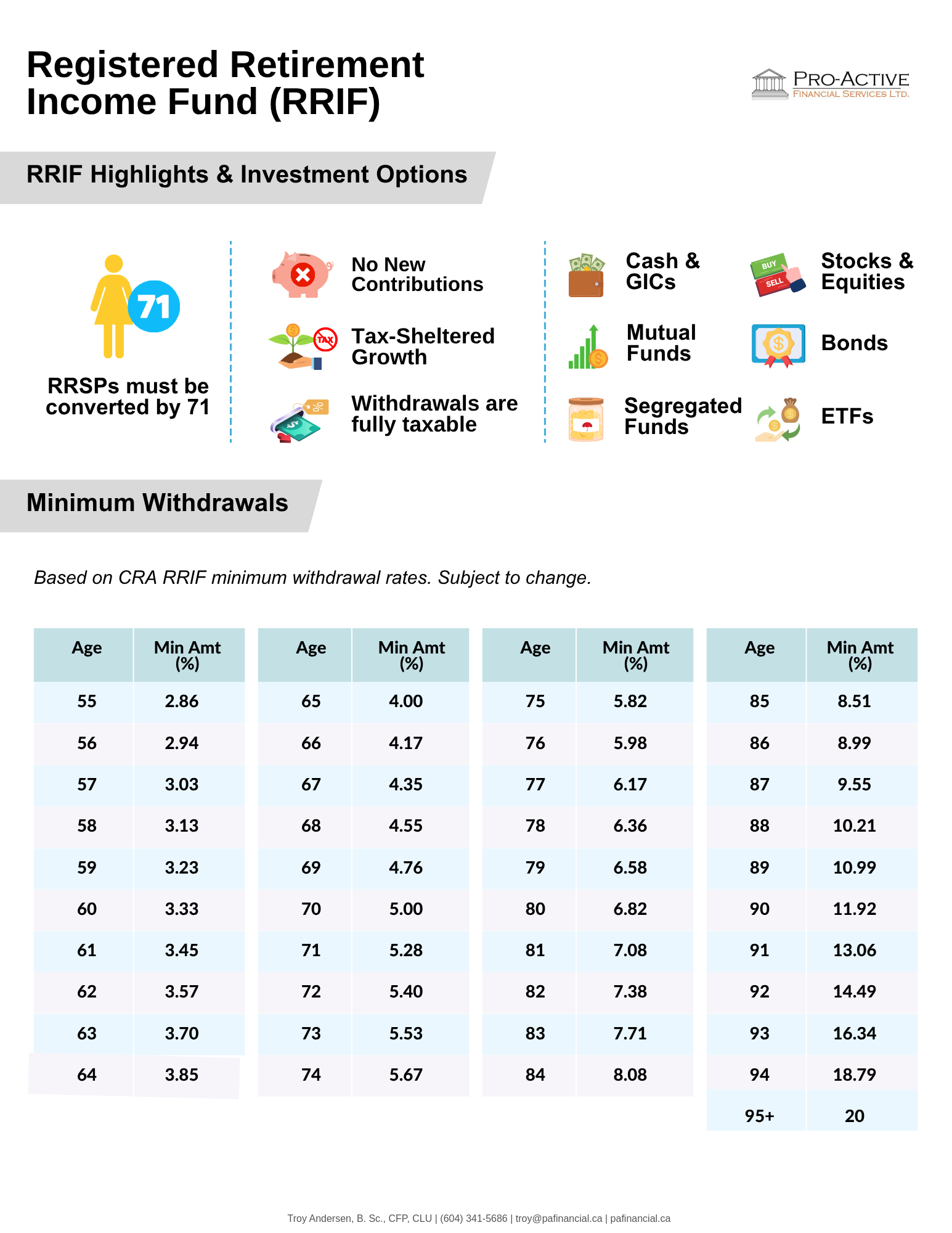

An RRIF is essentially the next stage of your RRSP. While an RRSP is designed for growing your retirement savings, an RRIF is designed for drawing income from them. You’re required to convert your RRSP into an RRIF (or an annuity) by the end of the year you turn 71, though you can convert earlier if it suits your needs.

Unlike an RRSP, you can’t contribute new money to an RRIF, and you’re required to withdraw at least a minimum amount each year. The investments inside your RRIF—like GICs, stocks, bonds, mutual funds—can continue to grow tax-deferred, but your withdrawals are taxable as income.

How do you transfer funds into an RRIF and what can you hold in it?

Converting your RRSP to an RRIF is straightforward. You open an RRIF account at your financial institution and transfer all or part of your RRSP into it. There are no taxes payable on this transfer itself.

Your RRIF can hold the same types of investments you had in your RRSP. That means you can continue to hold stocks, bonds, GICs, mutual funds, ETFs, and even cash. Many people simply carry their RRSP portfolio over to the RRIF unchanged, but it’s also an opportunity to adjust your investments to align with your income needs and risk comfort level.

Do you have to convert all your RRSPs at once?

If you have more than one RRSP account, you don’t have to convert all of them into an RRIF at the same time. You can convert just one account, a portion of your savings, or all of them—whatever works best for your situation.

Some people convert one RRSP early to supplement income while leaving the rest to grow. Others choose to convert all their accounts into one or more RRIFs for simplicity. Just keep in mind that by December 31 of the year you turn 71, all RRSP funds must be converted—whether into RRIFs, annuities, or withdrawn as cash.

You can also have more than one RRIF if you prefer to keep different investments or strategies separate. Each RRIF has its own minimum withdrawal based on its balance at the start of each year.

When should you convert your RRSP?

You must convert your RRSP into an RRIF no later than December 31 of the year you turn 71, but you don’t have to wait until then. Some Canadians choose to convert earlier, especially if they retire before age 71 and want to start drawing from their savings. Others may convert a portion of their RRSP to an RRIF early to smooth out taxable income over several years or to supplement other income sources.

Can you convert before age 71?

Yes. You can convert your RRSP to an RRIF at any age, as long as you’re ready to begin taking taxable withdrawals. For example, someone retiring at age 60 may decide to convert part of their RRSP to an RRIF and leave the rest in the RRSP to continue growing.

Converting your RRSP to a RRIF at retirement

By the end of the year you turn 71, you can no longer contribute to an RRSP — and you must convert it into an income stream. The most common way to do this is by transferring it into a Registered Retirement Income Fund (RRIF).

A RRIF keeps your investments tax-sheltered, but you’re required to withdraw a minimum amount each year, which is taxable. The minimum starts small and increases as you age.

Alternatively, you can purchase an annuity to guarantee income for life, but a RRIF gives you more flexibility to manage your investments and withdrawals.

Understanding RRIF Minimum Withdrawals

One of the key rules with an RRIF is that you must withdraw at least a minimum amount each year, starting the year after you open the account. This minimum is calculated as a percentage of the total value of your RRIF on January 1 each year, and the percentage increases as you age.

For example, if you are 71, the minimum is about 5.28% of your RRIF balance. At 80, it’s about 6.82%, and it continues to rise each year. You can always withdraw more than the minimum if you need to, but you cannot withdraw less.

If you’d like to lower your required withdrawals, you can choose to have the minimum based on your younger spouse’s age when you set up the RRIF. This option is helpful if you want to keep more money invested and reduce taxable income in the early years.

It’s important to plan these withdrawals carefully, especially if you don’t need all the income right away. Any funds you withdraw that you don’t spend can be invested in a TFSA or a non-registered account, depending on your available contribution room and tax strategy.

What if you don’t need the money immediately?

Even if you don’t need the income right now, you still have to withdraw at least the minimum each year. There’s no option to skip withdrawals altogether, but you can reinvest the money in a non-registered account or a TFSA if you have contribution room, allowing it to continue growing tax-efficiently.

How are RRIF withdrawals taxed?

Withdrawals from an RRIF are considered taxable income in the year you take them. Your financial institution will issue a T4RIF slip, which shows the taxable amount (Box 16) and any tax withheld. You report the taxable amount on line 13000 of your personal tax return under “Other income.” Any tax already withheld is credited when you file.

It’s a good idea to plan your RRIF withdrawals alongside other income sources (like CPP or OAS) to help manage your overall tax bill and avoid moving into a higher tax bracket.

What happens at death? Choosing a beneficiary and successor annuitant

When you open an RRIF, you can name a beneficiary or a successor annuitant. If you name your spouse as a successor annuitant, they can take over the RRIF without tax consequences, continuing to receive income from it. If you name your spouse or a financially dependent child as a beneficiary, the RRIF can be transferred to them with reduced tax consequences. If no beneficiary is named, the full value of the RRIF is included as income on your final tax return.

Naming the right person and understanding the tax implications is an important step in ensuring your retirement savings benefit your loved ones as you intended.

Your RRIF is more than just a requirement after age 71—it’s a flexible and valuable way to turn your hard-earned savings into a sustainable income stream. Planning how and when to convert your RRSP, understanding your minimum withdrawal requirements, and choosing a beneficiary thoughtfully can help you get the most out of your retirement savings.

If you’d like help reviewing your options, reach out—we’d be happy to guide you through the process.

Disclaimer: This article is for informational purposes only and does not constitute financial, legal, or tax advice. Always consult a qualified professional regarding your specific situation. We are not responsible for any actions taken based on this content.

Sources:

Government of Canada. Registered Retirement Income Fund: https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/completing-slips-summaries/t4rsp-t4rif-information-returns/payments/chart-prescribed-factors.html

Tax Tips. Registered Retirement Income Fund: https://www.taxtips.ca/rrsp/rrif-minimum-withdrawal-factors.htm