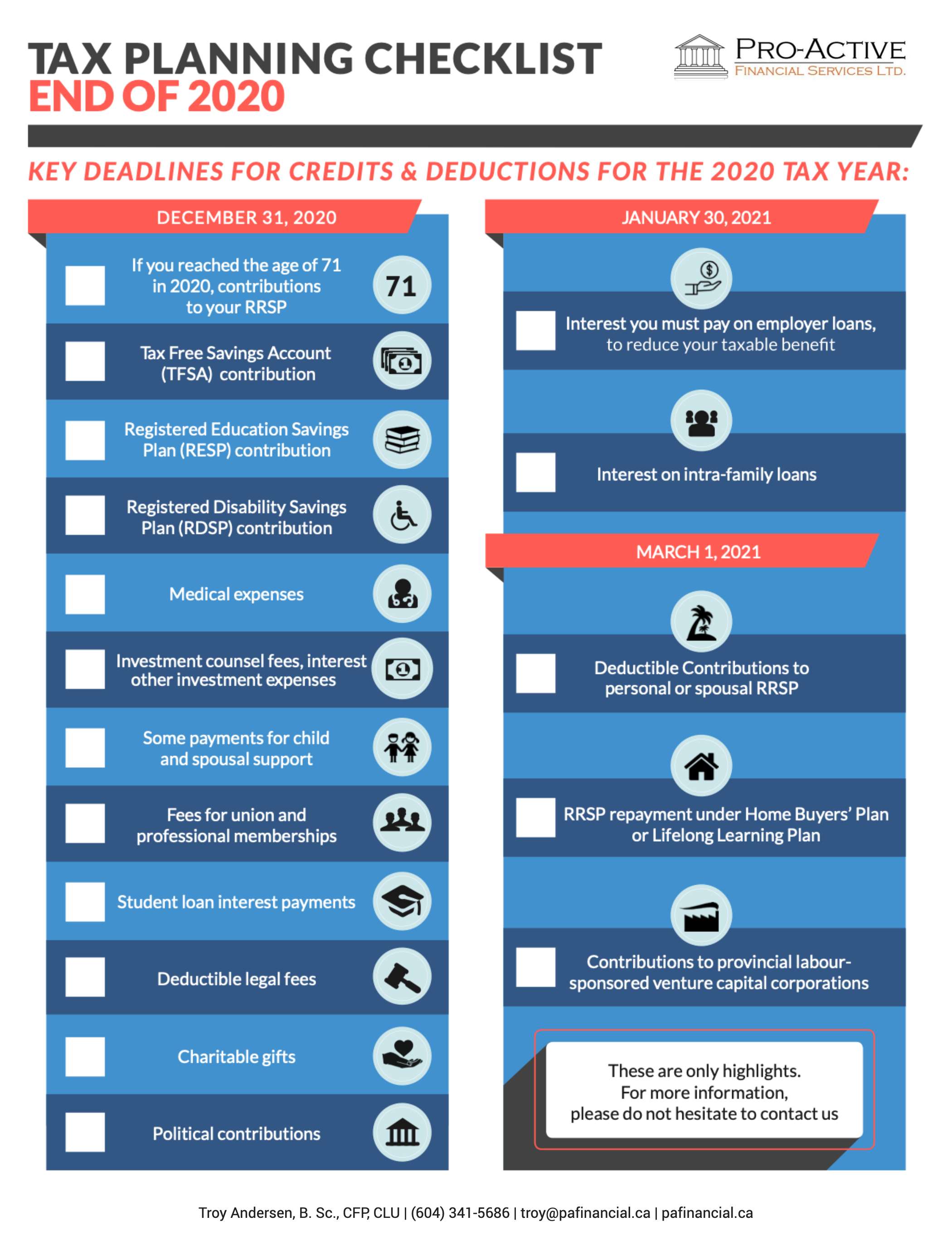

Extended COVID-19 Federal Emergency Benefits

On Friday, February 19, 2021, Prime Minister Justin Trudeau announced an extension to several of the COVD-19 federal emergency benefits. The goal of this extension is to support Canadians who are still being financially impacted by the COVID-19 pandemic.

The following benefits are impacted:

-

Canada Recovery Benefit

-

Canada Recovery Caregiving Benefit

-

Canada Recovery Sickness Benefit

-

Employment Insurance

Canada Recovery Benefit

The Canada Recovery Benefit (CRB) provides income support to anyone who is:

-

Employed or self-employed, but not entitled to Employment Insurance (EI) benefits.

-

Has had their income reduced by at least 50 percent due to COVID-19.

You can receive up to $1,000 ($900 after taxes withheld) a week every two weeks for the CRB. The recent changes now allow you to apply for this benefit for a total of 38 weeks – previously the maximum was 26 weeks.

Canada Recovery Caregiving Benefit

The Canada Recovery Caregiving Benefit (CRCB) helps support people who cannot work because they must supervise a child under 12 or other family members due to COVID-19. For example, a school is closed due to COVID-19 or your child must self-isolate because they have COVID-19.

You can receive $500 ($450 after taxes withheld) for each 1-week period you claim the CRCB. The recent extension made now allows you to apply for this benefit for a total of 38 weeks instead of the previous 26 weeks.

Canada Recovery Sickness Benefit

The $500 a week ($450 after taxes) Canada Recovery Sickness Benefit (CRSB) is also getting a boost. If you cannot work because you are sick or need to self-isolate due to COVID-19, you can now apply for this benefit for a total of four weeks. Previously, this benefit would only cover up to two missed weeks of work.

Employment Insurance

Finally, the government will also be increasing the amount of time you can claim Employment Insurance (EI) benefits. You will now be able to claim EI for a maximum of 50 weeks – this is an increase of 24 weeks from the previous eligibility maximum.

For full details, go to https://www.canada.ca/en/revenue-agency/campaigns/covid-19-update/covid-19-benefits-credits-support-payments.html